- Budgets and finance

- Carnegie UK

- 17 April 2026

- 18 minute read

Context

Carnegie UK’s Financing the Future programme has examined how governments can use public finance and fiscal processes to improve collective wellbeing. We brought together experts to discuss key challenges and successes across the UK and collaborated with researchers to understand citizens’ views on taxation and international practices for wellbeing budgeting. From this work, we identified important principles and practical approaches that governments across the UK can adopt to strengthen their strategies. However, we recognise that embedding wellbeing in budget processes requires more than one-off changes: it requires multiple, coordinated reforms alongside a culture change in collaborative working to improve governance and decision making in this essential area of public policy.

This paper on enhancing devolved borrowing powers is one of three connected policy provocations (with the others looking at second round fiscal effects and wellbeing cost benefit analysis respectively) that set out Carnegie UK’s current thinking in an important area of UK fiscal policy. Taken together, these three policy papers aim to prompt debate on improving how wellbeing is embedded in public finances.

This work is intentionally presented as a policy provocation. It does not represent a final or definitive Carnegie UK policy position on this issue. However, we believe there are issues worth articulating and exploring in this policy area. We welcome critique and feedback of the arguments put forward in this provocation.

Introduction

One of the key policy recommendations arising from the research and engagement strand of Carnegie UK’s Financing the Future Programme is a call for devolved governments across the UK to have increased borrowing powers. While a complex and significant policy proposal – and by no means a silver bullet – greater borrowing powers could enable devolved governments to invest more significantly in longer-term and more outcomes focussed approaches to policymaking. This in turn would support better collective wellbeing.

This paper sets out greater detail on the policy rationale and implications of this recommendation against the following headings:

- Executive Summary

- Section 1: Overview of existing borrowing powers in the UK

- Section 2: International comparisons of devolved borrowing frameworks

- Section 3: The Collective Wellbeing case for greater devolved borrowing powers

- Section 4: The Block Grant, Barnett formula and enhanced devolved borrowing

- Section 5: Improving fiscal policy coherence

Executive Summary

Carnegie UK’s Financing the Future programme highlighted a major constraint facing devolved governments across the UK: limited borrowing powers. Current devolved borrowing arrangements in the UK are tightly capped, inconsistent between jurisdictions, and weak by international standards. This restricts the ability of devolved governments to plan for the long term, to invest in prevention or the major socio-economic transitions required in the coming years (e.g: lifelong learning, climate mitigations etc), and to deliver policies that improve collective wellbeing.

Our core argument is that expanded borrowing powers, if designed carefully, could strengthen devolved governments’ capacity to invest in people, places and future generations, while maintaining UK-wide fiscal stability.

Why change should be considered

Current borrowing limits are restrictive: Scotland, Wales and Northern Ireland operate under low, cash-capped borrowing ceilings set by HM Treasury. These powers are currently mostly limited to capital, so cannot be used for resource funding for social initiatives with strong preventive impacts.

Even for capital investment, the current limits are not compatible with major long-term investment priorities such as climate transition and affordable housing.

International peers go further: Canadian provinces, US states, German Länder and Australian states all have greater borrowing autonomy, typically linked to GDP or governed by market discipline rather than small, fixed cash caps.

Collective wellbeing is held back: under the current system, devolved governments lack the fiscal tools to invest in ambitious initiatives that could improve wellbeing at scale.

Options considered

In examining this issue, a range of potential policy options were considered, including maintaining the status quo, enhanced devolved borrowing powers for capital investment, and enhanced devolved borrowing for both capital and resource investment. There are intricacies, opportunities and challenges associated with all options; on balance, Carnegie UK recommends that the option of enhanced borrowing powers for capital and resource investment should be considered. These powers should:

- Replace current borrowing cash caps with GDP-linked or rules-based limits.

- Be governed by transparent, jointly agreed fiscal rules, with input from independent fiscal bodies.

- Include safeguards to ensure equitable access across nations/jurisdictions.

- Be reported on openly to strengthen accountability and public trust.

Interaction with the Barnett Formula

Expanded borrowing powers would not have to alter the Block Grant or Barnett formula mechanics directly. However, they would interact politically and practically with block grant adjustments and spending choices. This underlines the need for stronger intergovernmental fiscal frameworks and transparency.

Expanded borrowing powers would not, on their own, resolve all fiscal policy challenges in the UK. But they would be a useful step towards a more mature and wellbeing-driven fiscal settlement for the UK. They would allow devolved governments to invest preventively, act on local priorities, and deliver for future generations, helping ensure that everyone has what they need to live well, now and into the future

Overview of existing borrowing powers in the UK

The political and policy context for current devolved borrowing powers cross the UK is complex and inconsistent.1

Scotland has the most extensive devolved borrowing powers, but all three devolved nations’ fiscal powers are capped tightly compared to international peers. The following is a top-level summary of the current/existing devolved borrowing powers across the jurisdictions of the UK.

UK Government

The UK government has full sovereign borrowing powers. It can issue bonds, Treasury bills, and other debt instruments in sterling and foreign currencies. Debt is managed by the UK Debt Management Office (DMO) under HM Treasury oversight. Borrowing covers both capital (infrastructure, investment) and resource/current spending (day-to-day costs like welfare, NHS).

Borrowing at a UK level is constrained by two main factors:

- Self-imposed fiscal rules (e.g. keep debt:GDP falling, limit borrowing for current spending), though these have been changed repeatedly by successive governments.

- External constraint is mainly market confidence (bond yields, credit rating agencies), not a legal cap.

UK borrowing sets the macroeconomic framework in which devolved and local authorities operate. All devolved borrowing is small and limited when compared with UK central borrowing.

Scottish government (as of 2023 Fiscal Framework)

- Resource borrowing: £600m annually with a £1.75bn cap (in 2023-24 prices). This resource borrowing is restricted to in-year cash management and dealing with the impact of forecast errors.

- Capital borrowing: £450m annually with a £3bn total cap (in 2023-24 prices) for investment in capital projects.

- Reserve: £700m cap (in 2023-24 prices).

- Restrictions: The UK Treasury sets the terms for this borrowing

Welsh government

- Resource borrowing: No equivalent facility (forecast error smoothing is provided via UK adjustments).

- Capital borrowing: £150m annually with a £1bn total cap for investment in capital projects.

- Reserve: £350m cap.

- Note that limits for Welsh Government borrowing are not currently indexed.

Northern Ireland Executive

- The Northern Ireland Executive has access to the Reinvestment & Reform Initiative (RRI), allowing up to £220m annually (as of 2024-25 and indexed from 2025-26 onwards) for capital.

- No meaningful resource borrowing powers.

- Fiscal stress issues are most often resolved via ad-hoc Treasury negotiations rather than rules-based borrowing.

English Combined Authorities / Mayoralties

- Borrowing powers are tied to prudential borrowing rules under the Local Government Act 2003.

- In practice, combined authorities and metro mayors can borrow only for capital investment (not day-to-day spending), and only in areas where they have devolved functions.

Examples

- Greater London Authority (GLA): Has substantial borrowing powers, capped by prudential borrowing rules. Can issue bonds (e.g. Transport for London has done so).

- Greater Manchester Combined Authority (GMCA): Can borrow for transport, housing and regeneration projects under devolved powers.

- West Midlands Combined Authority (WMCA) and others: Similar powers, subject to Treasury agreement, mainly for transport, housing, and economic development capital projects.

- English Combined Authority borrowing is subject to the Prudential Code (CIPFA), which aims to ensure borrowing is affordable, prudent and sustainable. Treasury approval is required for new borrowing powers under devolution deals and combined authorities have no power to borrow for general resource spending

Summary

The UK government primarily uses borrowing as a macroeconomic tool; devolved and local authorities use borrowing more as a micro-level investment lever. Treasury rules around borrowing ensure that devolved/local borrowing cannot materially affect UK-wide debt markets. The UK devolved borrowing framework is complex and inconsistent.

In the UK context, Scotland has relatively strong borrowing powers compared to Wales and Northern Ireland. However, when compared to other international examples (as detailed in the next section), devolved borrowing in the UK is small in scale and tightly controlled by the UK Treasury, minimising devolved autonomy.

Most nation states with significant devolved policy making give sub-national levels of government far greater borrowing and fiscal autonomy, with debt levels often governed by market discipline or GDP-based rules rather than small, fixed cash limits.

International comparisons of devolved borrowing frameworks

The following is a top-level overview of international examples of how other nation states with significant sub-national devolution approach devolved borrowing powers.2

Canada (Provinces)

- Canadian provinces can borrow widely, often issuing their own bonds (e.g. “Ontario bonds”).

- No hard federal caps on borrowing. Limits are set by financial markets and provincial credit ratings.

- For example, Ontario carries debt c40% of provincial GDP. This is far larger in scale than Scotland’s capped £3bn potential capital investment borrowing powers.

United States (States)

- US States generally cannot run persistent operating deficits as they mostly operate to balanced budget rules.

- US States can however borrow freely for capital projects, often via municipal bonds. US states have significant fiscal and borrowing autonomy. For example, California’s bonded debt is over $70bn.

- US States with strong credit ratings can borrow on highly favourable terms

Germany (Länder)

- The German federal system historically allowed Länder to borrow.

- Post-2011 constitutional reform introduced the “Schuldenbremse” (debt brake): Länder must balance budgets but can borrow in downturns or emergencies.

- German Länder borrowing powers are much wider than UK jurisdictions as their borrowing ceilings are linked relative to GDP, not fixed cash amounts.

Australia (States)

- Under the Australian Constitution, states are sovereign within their own jurisdictions. Unlike UK devolved governments, Australian states have the power to borrow without constitutional caps.

- There is no UK-style Barnett formula: instead, states receive GST distributions (via the Commonwealth Grants Commission) and tied grants, but they can also raise debt directly by issuing bonds directly into financial markets.

- Each state runs its own central borrowing authority (e.g. state treasuries) and these entities issue state bonds which trade in capital markets alongside Commonwealth bonds. Australian state borrowing is substantial, with state debt stocks often exceeding $100bn, especially NSW and Victoria.

Summary

Compared to these international examples the devolved borrowing caps in the UK are small, limited and tightly controlled by the central UK Treasury.

The Collective Wellbeing case for enhanced devolved borrowing powers

At Carnegie UK, collective wellbeing means everyone having what they need to live well now and into the future.

We believe that collective wellbeing happens when social, economic, environmental and democratic wellbeing outcomes are seen as being equally important and are given equal weight in policy and decision making. We refer to this as the SEED model:

- Social wellbeing: We all have the support and services we need to thrive.

- Economic wellbeing: We all have a decent minimum living standard.

- Environmental wellbeing: We all live within the planet’s natural resources.

- Democratic wellbeing: We all have a voice in decisions that affect us.

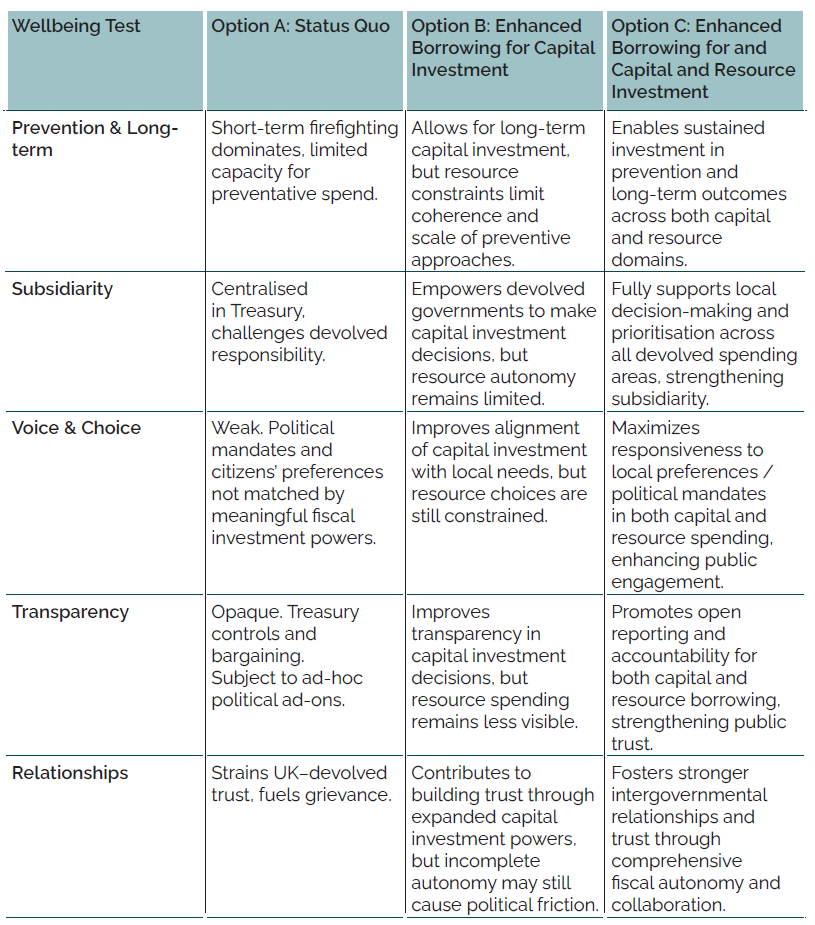

We also know from our decades of work that there are certain policy conditions and practices which can build and improve the wellbeing of people and places. We call these our Wellbeing Policy Tests:

- Focus on prevention and the long-term: Build processes that support long-term thinking while prioritising prevention in policymaking and services.

- Support subsidiarity: Prioritise local decision-making, reflecting the needs and priorities of individual communities. Support local people to improve their own wellbeing.

- Give people voice and choice: Put conversations and deliberation between different communities, sectors and professions at the centre of decision-making.

- Enhance transparency: Give open access to knowledge and evidence to support better policymaking.

- Recognise relationships: Understand the importance of human relationships and social connections in delivering better public policy and services.

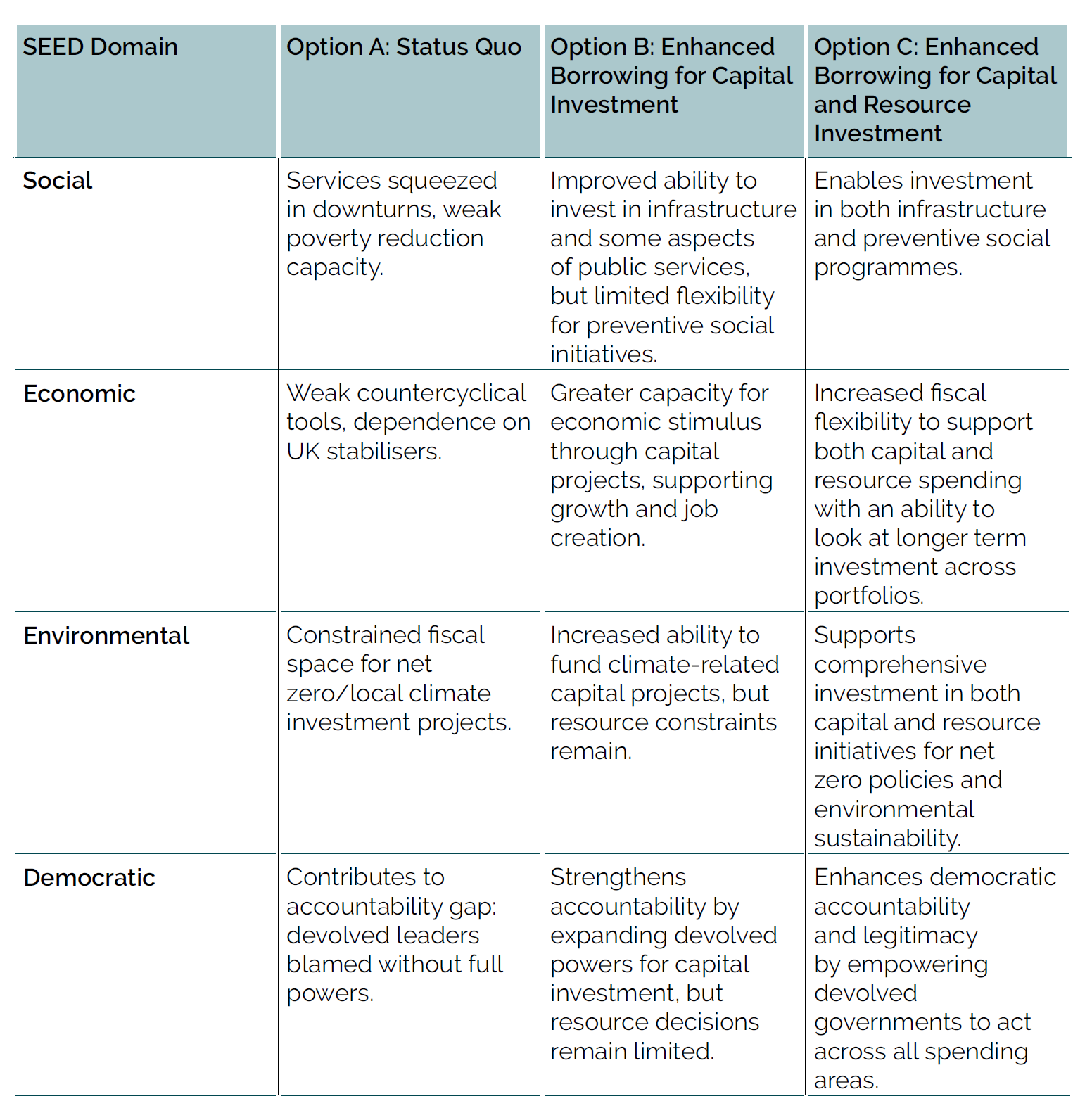

Assessing options for devolved borrowing powers

In looking at established policy positions for enhanced devolved borrowing in the UK three broad categories of options emerge:

Option A: Status Quo: current limits and existing Treasury controls.

Option B: Enhanced borrowing powers for capital investment: higher limits with greater ability to invest in capital initiatives.

Option C: Enhanced borrowing for capital and resource investment: higher limits with greater ability to invest in both capital and preventative resource initiatives.

Assessment by Carnegie UK SEED domain:

Assessment by Wellbeing Policy Tests:

In this assessment model Option A: Status Quo Mostly fails across both wellbeing outcomes and policy tests. It entrenches short-termism, undermines subsidiarity, and contributes to a corroding of democratic accountability.

Option B: Enhanced Borrowing for Capital Investment delivers improvements over the status quo but falls short of meaningfully greater fiscal empowerment. While it enables devolved governments to better respond to infrastructure needs and enhance public services through increased capital investment, limitations on resource borrowing continue to restrict flexibility in addressing recurrent spending priorities. Consequently, the ability to deliver holistic wellbeing outcomes across all policy areas is constrained.

As shown in the tables above, Option C for enhanced capital and resource borrowing enables sustained investment in both infrastructure and preventive social programmes, supporting holistic policy approaches to improving collective wellbeing. It encourages long-termism, it is subsidiarity-friendly and transparent. It balances devolved responsibility with macroeconomic stability in a shared UK framework.

Summary

Against Carnegie UK’s criteria, Option C (Enhanced Devolved Borrowing Powers for Resource and Capital Investment) emerges as the preferred fit with both our model of collective wellbeing and wellbeing tests. It balances flexibility and responsibility, allows greater prevention-focused investment across a wider range of policy areas from governments across the UK as well as strengthening subsidiarity and improving trust and transparency.

The Block Grant, Barnett Formula and enhanced devolved borrowing

Block Grant

The Block Grant is the main source of funding for devolved governments in the UK (Scotland, Wales, Northern Ireland) 3. It is set and paid annually by the UK Treasury. The Block Grant pre-dates the devolution of additional tax powers in recent years and gives the devolved administration freedom to make decisions on spending within its devolved competence without reference to the UK Government.

The Block Grant is adjusted annually by the Barnett Formula and tax and spending related Block Grant Adjustments (BGAs).

Block Grant Adjustments (BGAs)

Since some taxes are either fully or partially devolved (e.g. Scottish income tax, Welsh landfill tax), the UK Treasury reduces the block grant by an amount reflecting the tax revenues foregone by the UK. This means devolved governments keep the revenues they raise from devolved taxes but lose an equivalent portion of the block grant.

The Barnett Formula

The Barnett Formula is the mechanism used by the UK Treasury to adjust the block grants allocated to the devolved administrations (Scotland, Wales, Northern Ireland).

The Barnett Formula does not determine the absolute size of devolved budgets. Instead, it determines changes (increases or decreases) to those budgets when UK government departments’ spending on comparable services in England changes.

Each year and at major fiscal events, such as UK Budgets, the Barnett Formula applies the following calculation:

- {Change to Devolved Block Grant} = {Change in UK Department Spending} x {Comparability Percentage} x {Population Share]

Change in UK Department Spending: The increase (or decrease) in planned expenditure for a given Whitehall department (e.g. Health, Transport, Education).

Comparability Percentage: A Treasury assessment of how far the UK department’s function overlaps with devolved responsibilities.

- 100% if fully devolved (e.g. Health, Education).

- Lower if partly devolved (e.g. Transport, Agriculture).

- 0% if not devolved (e.g. Defence, Foreign Affairs).

Population Share: The devolved nation’s population as a proportion of England’s (or England + England and Wales, depending on coverage). Based on ONS/ONS-adjusted mid-year population estimates.

The formula is applied separately for Scotland, Wales, and Northern Ireland, and for each UK government department. It determines the year-on-year change (the “consequential”) in the devolved block grant by applying population and comparability proportions to changes in UK departmental spending.

The Barnett formula responds to UK spending decisions, not to devolved borrowing or devolved spending decisions.

Policy and political implications of these proposals

Distributional and no-detriment tensions

- Because Barnett is population-based and only tracks changes in UK spending, it can potentially leave devolved nations under- or overcompensated for specific needs (e.g: Scotland’s higher net-zero costs).

- Expanded borrowing powers would give devolved governments scope to close that gap but would not change the Barnett arithmetic that determines consequentials.

- Politically, this could create friction between the nations and regions of the UK. Devolved governments borrowing to make up shortfalls may argue they are compensating for Barnett’s shortcomings. Westminster politicians may counter that devolved borrowing is their choice. This could lead to issues around political blame and legitimacy disputes.

Equalisation and jurisdictional fairness

- The Barnett formula is not in itself an equalisation mechanism. It produces per-person changes, not needs-based allocations. There are additional needs based fiscal mechansims that exist for Wales and Northern Ireland to supplement the Barnett Formula. 4

- Expanded devolved borrowing powers could help correct place-based underfunding, but without formal equalisation or transitional support it risks widening regional inequalities.

- For example, richer tax bases could potentially borrow more cheaply for growth projects, less affluent areas may not be able to access the same borrowing rates and therefore invest less.

- This could undermine the “no detriment” or taxpayer fairness ambitions the Smith Commission tried to balance.

Institutional complexity and transparency

- More devolved borrowing would increase fiscal policy complexity across the UK (borrowing, BGAs, reconciliations, consequentials etc).

- Without greater collaboration and openness, stronger institutions and public reporting this risks further eroding coherence and democratic accountability.

Overview

From a technical point of view, increasing and enhancing devolved borrowing powers does not change the Barnett formula directly. However, both politically and in practice it would create a set of institutional frictions and second-order effects (duplication risk, distributional tension, market signalling) that would have to be managed with improved coherence and coordination mechanisms, offsets, and transparency.

Improving fiscal policy coherence

Examining how enhanced borrowing powers can be devolved across the UK is an important part of ensuring policy makers can access the fiscal levers needed to deliver improvements to our collective wellbeing. This would represent an important step towards more mature, more coherent and less centralised fiscal relationships across the UK.

Delivering this requires a strategic commitment to strengthening fiscal policy coherence across the UK’s complex landscape of devolved and central government relationships. Practical steps must be taken that acknowledge the existing complexity of the UK’s fiscal arrangements and actively reinforce institutional alignment. Consideration should be given to the standardisation of devolved fiscal powers and reporting wherever possible.

Enhanced frameworks

- The first essential in improving fiscal policy coherence in the UK is the establishment of enhanced institutional frameworks. This would likely include the development of clear rules and protocols for fiscal data sharing, harmonisation of public financial reporting standards, and the regular convening of intergovernmental fiscal forums. Such structures must be built on mutual trust and accountability, with each administration equipped to both articulate and scrutinise borrowing strategies, risk management, and long-term fiscal planning.

Strengthening transparency

- Transparency is foundational to improving fiscal policy coherence. By making data on borrowing, block grant adjustments, and Barnett consequentials available in user-friendly formats, public understanding and democratic accountability can be enhanced.

Ensuring integrity of the Barnett Formula

- Enhanced devolved borrowing powers do not directly alter the Barnett formula, but they would require continuous monitoring of second-order effects. It is likely that second-order economic and fiscal effects would grow as a result of enhanced borrowing powers, as such, there would be a need to review the existing mechanisms for assessing these to ensure that the ‘no detriment’ principle can be properly met.

Embedding continuous improvement

- Enhancing devolved borrowing powers emphasises the importance of a flexible, learning-driven approach to policy making. Regular independent reviews of the UK’s fiscal frameworks should be embedded, with a focus on improving overall operational coherence and a willingness to adapt rules and processes in response to evolving political and economic circumstances. Improved fiscal policy coherence is not a static achievement but an ongoing process.

Summary

This recommendation for enhanced devolved borrowing powers hinges on a willingness to focus on fiscal policy coherence, invest in robust institutions, transparent practices and collaborative relationships across jurisdictions. By prioritising these elements, the UK can transform the challenges of devolved borrowing into an opportunity to create a more accountable, and resilient fiscal policy landscape that enables decision makers to better invest in long-term improvements for collective wellbeing.

- Devolved Administration Funding and the Barnett Formula (HM Treasury 2021) ↩︎

- Options for reforming the devolved fiscal frameworks post-pandemics (IFS 2021) ↩︎

- The Barnett Formula and Fiscal Devolution (UK Parliament research briefing 2025) ↩︎

- Institute for Government explainer on the Barnett Formula ↩︎

Help us make the case for wellbeing policy

Keep in touch with Carnegie UK’s research and activities. Learn more about ways to get involved with our work.

"*" indicates required fields